A Critical First Step to Outsized Net Net Returns

When it comes to making large investing profits, one factor stands out above all the rest.

Most investors look for hot stocks or stocks that are expected to do exceptionally well over the next month or year. They spend their time pouring through message boards or consuming the drabble of Wall Street pundits then jump on stocks that have had good growth or are currently being hyped. These are the Starbuckses or Tesla Motors of the world -- great promising companies that investors generally recognize as great or promising and are willing to pay top dollar for. By contrast, most investors ignore solid, stable, slow growing, dividend paying stocks or stocks of companies that are currently facing significant business problems.

I used to be in the same camp. Back when I was struggling to find my footing as an investor I tried my hand at buying growing companies but had little success. I spent my time assessing the growth history of companies and trying to imagine how things would unfold in the future. While I had some successes, after a number of years my portfolio was obviously not growing and I was pretty much wasting my time researching stocks.

Fill your portfolio full of high potential, low risk, net net stocks. Click Here.

That situation changed when I started applying the principles of Benjamin Graham. If you have already read the article My NCAV Investment Scorecard, you should already have a solid picture of what I look for in net net stocks. All of those factors have a purpose and all add value to the selection process. Despite that, one factor stands out above the rest in terms of determining the returns you can achieve as an intelligent investor. That factor is the price you pay.

Price is What You Pay, Value is What You Get.

The whole idea behind value investing is that investors profit by paying less for a company than it is worth. When it comes to making large profits in value investing, price is key. Essentially, investors lock in future profits when they buy since buying determines the spread between price and value as well as the amount the stock has to rise to become fairly valued.

And that's specifically what I'm talking about when I talk about price -- price relative to value. A low stock price doesn't necessarily mean anything for investors. Sure, volume can be higher on lower priced stocks but a high volume stock can lose money just as easily as a low volume stock can rocket upwards in price.

"Everyone I know that followed Ben had one thing in common, they never lost money. Because we were taught to buy so cheap, that no matter what happened, we were fine." — Marshall Weinberg

When it comes to net net stock investing, the discount at which you buy at is critically important. That's why I always try to buy below a 50% discount to intrinsic value.

1/3rd Discount to Intrinsic Value a Minimum Entrance Requirement

Of all the studies I've looked at when it comes to net net stock investing, every single one of them is clear -- the lowest priced net net stocks consistently outperform their higher priced counterparts.

Jae at Old School Value ran two tests looking at the raw portfolio returns of net net stocks (you can read the first test here, and the second test here). Jae's site is great -- it's one of the resources that ultimately sold me on adopting a net net stock strategy.

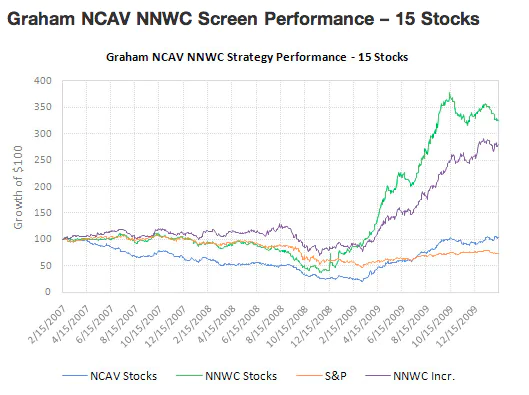

In the first backtest, Jae looked at net net stocks that traded below NCAV and compared those to NNWC stocks and the S&P 500. NNWC stocks are a special type of net net stocks. Instead of taking the current assets at the value they're quoted at on the balance sheet, those assets are market down to add conservatism.

This study utilized portfolios made up of 15 stocks. Portfolios were split between NCAV stocks, NNWC stocks, NNWC increasing stocks (NNWC stocks where the firm's NNWC value was increasing). Looking at the results, it's clear just how much the NCAV portfolio under-performed. NNWC stocks and NNWC increasing stocks thumped the market by a wide margin while NCAV stocks under-performed the market for 2 1/2 years before just squeaking past the S&P 500 at the end of the 3 year period. Depressing.

At first glance investors might conclude that NCAV stocks aren't worth the effort. Notice, though, that the NCAV stocks in the study are only priced below NCAV and don't include a margin of safety. That is to say, the NCAV portfolio doesn't require a specific discount to intrinsic value, each stock's NCAV.

Jae ran another study looking at what would happen if he only included stocks trading below a 1/3rd discount to NCAV. The results were quite different. Instead of under-performing, NCAV beat NNWC stocks by 50% from 2001 to 2004 while the S&P 500 inched along to finish the period slightly underwater. As you can see, the performance of net net stocks from 2001 to 2004 was 600%!

Jae also looked at the 2004 to 2007 and 2007 to 2010 periods. In the 2004 to 2007 period NCAV stocks under-performed NNWC stocks 150% to 50%. More notably, though, they also under-performed the S&P 500 by ~ 5%. As you'll see at the conclusion of this overview of Jae's study, this 3 year period of underperformance was well worth it.

From 2007 to 2010 NNWC and NCAV returns were locked together, coming in just under a 100% return. That's a 100% return in just 3 years! In comparison, the S&P 500 typically doubles in 9 years...

Take a moment and compare the performance of NCAV stocks on the chart directly below to the first chart displayed above covering the same period. The difference is striking, isn't it?

All together NNWC stocks just barely out performed NCAV stocks but both NCAV and NNWC stocks thundered past the market by a wide margin. Adding up the performance from period to period shows that the model portfolio would have beaten the market by over 1000%!

Jae's series of studies shows just how important it is to buy net net stocks at a large discount to intrinsic value. The returns of portfolios that include a 1/3 margin of safety and those that exclude it are drastically different. That being said, what happens when we demand an even greater discount to NCAV?

Buy Low, Rake in the Cash.

There have been a few studies that look at the effect that a wider price-value discrepancy has on portfolio returns.

Probably the most significant was a study published by Oppenheimer in 1986, titled "Ben Graham's Net Current Asset Values: a Performance Update." In the study, Oppenheimer tests Graham's net net stock strategy against the NYSE-AMEX index and the Ibbotson and Sinquefield Small-Firm Index. He writes,

The NAV criterion indicates that the investor is to purchase all securities with a price that is two-thirds or less of NAV. A question of some interest is whether the degree of undervaluation is related to subsequent performance. To examine this, we calculated for each security purchase price as a percentage of NAV. Each year, we divided the population into quintiles according to this variable and analyzed mean returns as well as risk-adjusted performance. The results are presented in Table VI.

The conclusion is clear-cut. Returns and excess returns can be rank-ordered, with securities having the smallest purchase price as a percentage of net asset value having the largest returns. It appears that degree of undervaluation is important: The difference in both mean return and risk-adjusted return between quintiles 1 and 5 is over 10 per cent per year.

Put another way, the results of stocks trading at the lowest price-to-NCAV returned over 50% more than firms with the smallest discount to intrinsic value.

How Net Net Stock Investors Should Proceed

The evidence is in and the conclusion is clear -- buying net net stocks at the steepest discount to intrinsic value significantly outperforms not only the general market but also other NCAV portfolios. If an intelligent investor wants to achieve the highest possible returns using a NCAV stock strategy then it would be wise to choose the cheapest stocks possible.

For my own portfolio, I screen for quality quite rigidly while also demanding very large discounts to NCAV. That makes investing in net net stocks more difficult but also -- I assume -- far more profitable. If an investor wants to do nothing else but purchase stocks that fit a specific set of characteristics then the returns will be very good over the long-term. If an intelligent investor wants to achieve the highest possible returns, however, then looking at the cheapest stocks is a great first step.

The catch, of course, is that great net net stock investment candidates can be tough to find. You can solve this problem by signing up for full Net Net Hunter membership. Not only do we have over 450 net net stocks to look at but we also dig through the listings to identify the best investment candidates. The money you could make off of even just one international net net stock would be enough to pay for full membership access for years.

Not ready for full membership? That’s fine. Just sign up for the free net net stock essential guide in the box below this article. No commitment, no obligation, and we keep your email address 100% confidential. Don’t wait. Sign up now so you can start making over 25% annual returns through net net stocks.